Published on 11/30/2016 | Strategy

One of the most hard coded matter in the tech and finance industry is Blockchain and usage of IoT (Commonly known as "Internet of Things") in the smart devices.

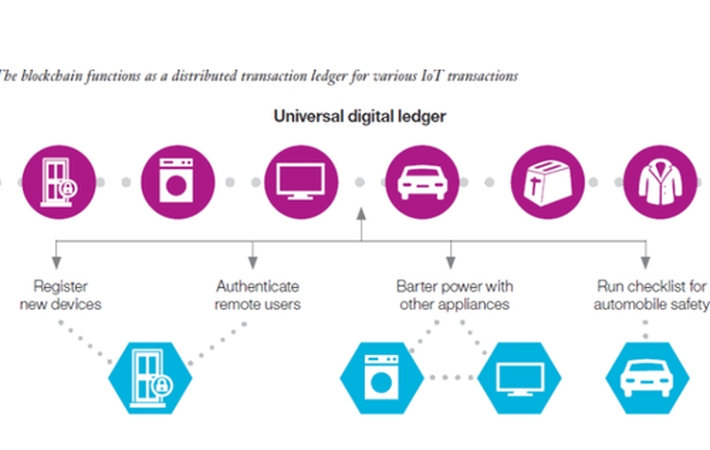

Blockchain: A distributed digital public ledger being recorded and validated by group of users anonymously. A peer to peer cryptographic network, with no central governance and no censorship by individual or any country.

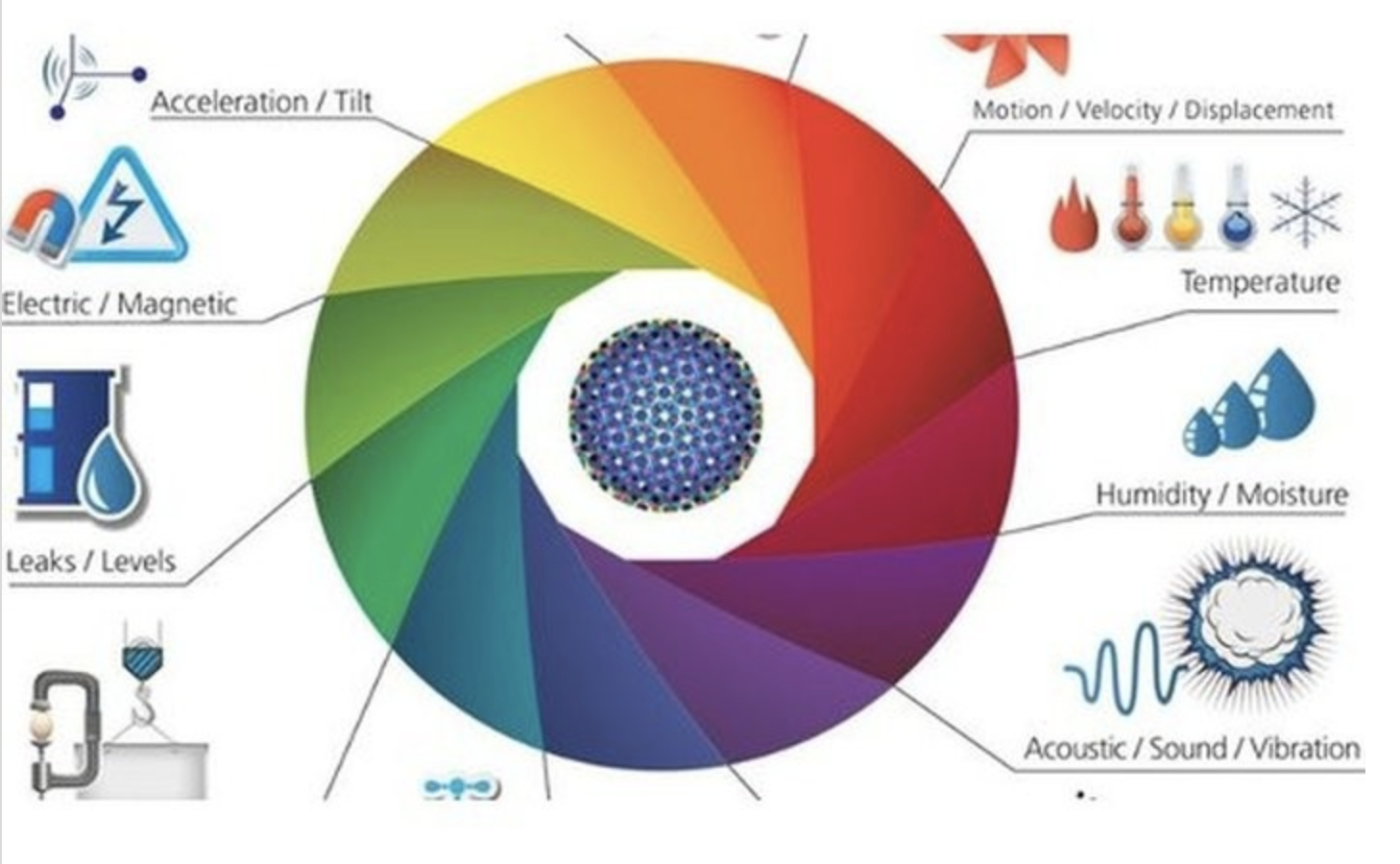

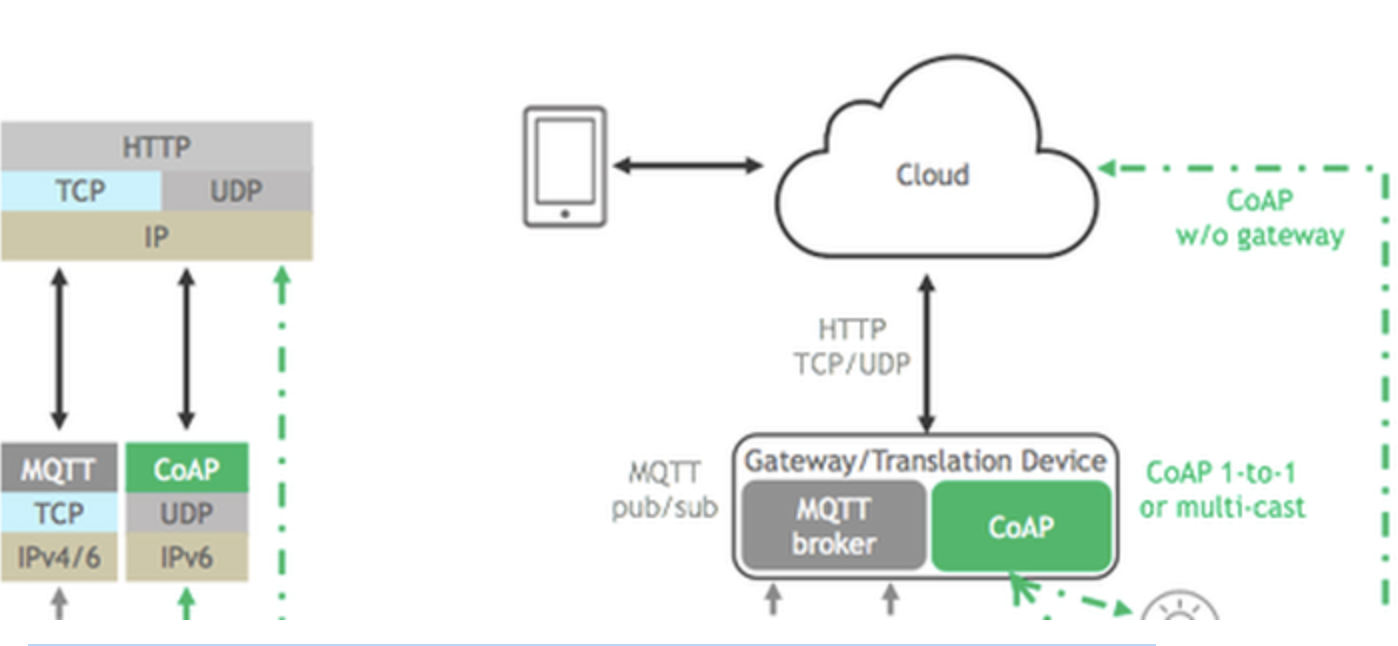

IoT: Your devices are inter-connected to each other through internet. It can be any device. For instance- television, refrigerator, washing machine, air-conditioner, oven, light bulb, door lock, alarm, biochip, vehicle, elevator, sensor and the list goes on...

Blockchains offer a way to verify and order transactions in a distributed ledger, a record of consensus that is validated and held within a network of separate nodes. Entries can be altered but not deleted from a blockchain based distributed ledger. Maintenance and validation of the distributed ledger is performed by a network of communicating nodes that run dedicated software that replicates the ledger among participants in a peer-to-peer network. All transactions have an audit-able trail and a traceable digital fingerprint. The data on the ledger is pervasive and persistent, creating a reliable “transaction cloud” where transaction data cannot be lost.

The number of objects able to record and transmit data to other objects is continually rising. 50 billion objects are expected to be linked to the internet by 2020. This network of connected devices creates continuous streams of data which can increase efficiency across a wide range of business practices. Many applications already exist: in transport, tracking when a bus will arrive; in pharmaceuticals, monitoring temperature-sensitive products; and in insurance, monitoring the driving style of car owners to preferentially price premiums for safer drivers. As the cost of sensors and data transmission continues to reduce, we are reaching a tipping point where commercial use of the IoT will take off.

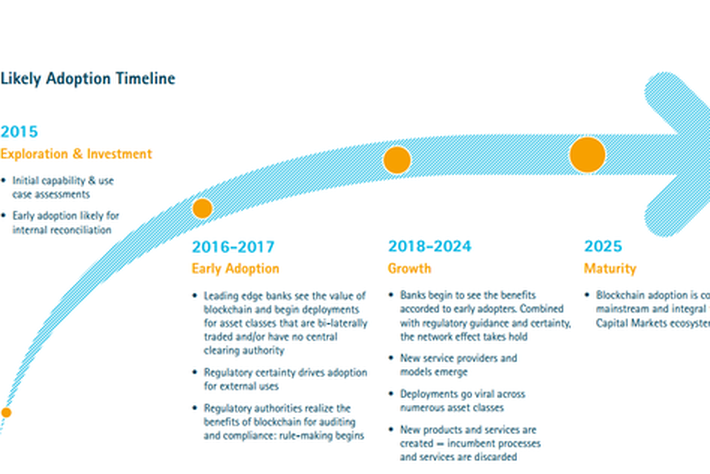

In mid-2015, Accenture published a report on the potential impact of blockchain technology on the investment banking industry. Since then, interest in and funding for this type of financial technology (FinTech) have grown exponentially. An estimated $75 million was invested in blockchain efforts specific to capital markets in 2015, up from $30 million in 2014. By 2019, that figure is expected to reach $400 million, amounting to a compound annual growth rate (CAGR) of 54 percent - forecasts that may prove conservative.

Global trade finance is a complex process. A dizzying number of manual checks must be carried out to verify the legitimacy of a client, its trading partners and the goods that change hands. Most checks require the physical presence of a person, and the administrative work conducted by bank middle offices is overwhelmingly paper-based. The high cost of this process restricts access to trade finance for smaller businesses and especially those in developing economies whose credit-worthiness is difficult to establish.

In addition, a number of groups have announced plans to explore blockchain technology for banks. The Linux Hyperledger Project aims to “develop an enterprise-grade, open-source distributed ledger framework and free developers to focus on building robust, industry-specific applications, platforms and hardware systems to support business transactions.” Similarly, an R3-led consortium of more than 40 institutions is developing blockchain-enabled solutions specifically for capital markets. Even major central banks are exploring how to leverage opportunities created by blockchain technologies.

SWIFT, the operator of the platform that facilitates the global inter-banking system, has recently revealed details about their blockchain project; a platform for its member banks that will facilitate cheaper, more effective and quicker operations and provide smart contracts to clients. SWIFT has shared details of its blockchain network, pointing to five separate nodes spread across the world, for its PoC tests. Nodes were installed in three participating banks in Sao Paolo, Frankfurt and Sydney, with two more nodes in SWIFT offices at California and Virginia.

SWIFT Labs’ R&D chief Damine Vanderveken stated:

"SWIFT has been targeted in the press as a legacy incumbent that will be doomed by DLT (Distributed Ledger Technology or Blockchain tech). But we believe SWIFT can leverage its unique set of capabilities to deliver a distinctive DLT platform offer for the community."

Bitcoin was the first to introduce blockchain technology back in 2010, more and more alt coins are now appearing with rich feature in the current economy while creating stronger and wider ecosystem as whole. One of the most transacted alt coin is Ether; project name or blockchain name is Ethereum. Some say it's the upgraded version of Bitcoin. With Ethereum you can write smart contract with coding knowledge and set things at play. Having said that various organizations are raising funds for their projects through crowdfunding. Method is simple, like Initial Public Offering. But with different name called IPCO/ICO (Initial Public Coin Offering). The DAO token was one of the biggest and fastest crowdfunding raised around $163 Million in equity value.

You may all get pretty excited with this emergent technology, however this whole thing is quite volatile. Mt. Gox, which was once the world's largest exchange for the decentralized crypto currency, filed for bankruptcy protection in February 2014, when it was reported that 850,000 bitcoins, worth $450 million at the time, had disappeared or been stolen by hackers. Attack on blockchain network is new challenge which has to be overcome in order to thrive.

Recognizing blockchain technology’s potential in the capital markets ecosystem, Santander begins to invest in FinTech and assess its impact:

July 2014: Santander InnoVentures, a $100 million incubator fund for FinTech innovation, is launched.

June 2015: A white paper titled “FinTech 2.0” highlights distributed ledgers in conjunction with the Internet of Things (IoT), identifying between 20 and 25 use cases that could save banks between $15-20 billion annually by 2022.

Regulatory acceptance: The most mature distributed ledger blockchains to date are cryptocurrencies, and regulators have reacted positively to them, even licensing a number of exchanges. The “smart contract” debate is really a question of where the business logic for transactions should live. With millions of contracts executed daily, it is daunting to consider a scenario where the business logic code would be attached to individual transactions.

All signs suggest that blockchain-enabled distributed ledgers are coming. The question is: are you ready?

This article was originally posted on LinkedIn.